How Much Income Do You Need to Buy a Home in Boulder, Colorado?

For a practical July 2026 benchmark, a household buying near Boulder’s recent all-home median sale price of $854,489 with 20% down may need roughly $202,000 to $217,000 in gross annual household income. The lower figure keeps the illustrated monthly housing cost near 30% of gross income; the higher uses a more conservative 28% planning ratio. That estimate assumes a 30-year loan at 6.49%, a property-tax proxy based on Boulder County’s published example, no HOA, and a clearly hypothetical $300 monthly homeowners-insurance allowance. Actual lender qualification may be higher or lower.

The likely reader is a first-time or relocating buyer trying to convert Boulder prices into a realistic salary target. The key is to calculate the total property-specific monthly cost, not just principal and interest. This guide shows the numbers, explains what changes them, compares Boulder with nearby markets, and identifies programs that may reduce cash-to-close.

The income needed for a Boulder home is usually about $200,000-plus at the recent median

The clearest answer is a range, because income needs change with price, down payment, interest rate, debt, HOA dues, taxes, and insurance. The following scenarios use the July 9, 2026, Freddie Mac average of 6.49% for a 30-year fixed mortgage. Freddie Mac’s benchmark is based on conventional, conforming purchase applications with 20% down and excellent credit, so it is a market reference rather than a personal quote.

| Hypothetical purchase | Down payment | Loan amount | Estimated monthly housing cost* | Income at 30% housing ratio | Income at 28% housing ratio |

|---|---|---|---|---|---|

| $500,000 condo or townhome | 20% / $100,000 | $400,000 | $3,333 | $133,000 | $143,000 |

| $854,489 Boulder median, all home types | 20% / $170,898 | $683,591 | $5,056 | $202,000 | $217,000 |

| $1,250,000 detached-home example | 30% / $375,000 | $875,000 | $6,568 | $263,000 | $282,000 |

*Illustrative estimates only. The calculations use a 30-year fixed mortgage rate of 6.49%, principal and interest, a property-tax proxy based on Boulder County’s published example, and hypothetical insurance and HOA assumptions. The estimates exclude closing costs, utilities, maintenance, mortgage insurance, and special assessments. Actual payments and income requirements depend on the property, loan terms, borrower qualifications, taxes, insurance, HOA obligations, and other debts.

The City of Boulder describes housing as affordable when a household spends less than 30% of income on housing. That is a housing-policy benchmark, not a mortgage approval rule. A buyer may qualify above that level, but qualification and comfortable affordability are not the same decision.

A useful sensitivity rule is that every additional $100 per month in HOA dues, insurance, taxes, or another required housing expense calls for about $4,000 more annual income at a 30% ratio, or about $4,286 more at 28%.

Mortgage qualification and comfortable affordability are different calculations

A lender’s debt-to-income ratio, or DTI, divides monthly debt payments by gross monthly income. It generally includes the proposed housing payment plus recurring obligations such as auto loans, student loans, credit-card minimums, and other debts shown in underwriting. Different lenders and loan programs use different limits.

Fannie Mae’s current Selling Guide can permit DTI ratios up to 50% for some Desktop Underwriter casefiles, but that does not mean every borrower qualifies at 50% or should plan to spend at that level. Automated underwriting also evaluates credit history, reserves, reliable income, and other risk factors.

For planning, use two screens:

- Housing-cost screen: Keep the proposed total housing payment within a percentage of gross income that leaves room for taxes, savings, childcare, travel, healthcare, and other priorities.

- Total-debt screen: Add the housing payment to all recurring monthly debts, then divide by gross monthly income.

For example, a buyer with a $5,056 illustrated housing payment and $1,000 in other monthly debt has $6,056 in total monthly debt. At a 36% planning DTI, that would require about $202,000 in gross annual income. At 43%, the mathematical figure is lower, but the household would have less cash-flow margin. These are planning examples, not underwriting promises.

Interest rate and down payment also move the answer quickly. On the $854,489 median-price example, principal and interest is about $4,316 at 6.49% with 20% down. At 5.49%, it would be about $3,877; at 7.49%, about $4,775. A one-percentage-point rate change therefore shifts the payment by roughly $440 to $460 per month in this example.

With only 10% down, principal and interest rises to about $4,856 before adding mortgage insurance. The Consumer Financial Protection Bureau notes that mortgage insurance is typically required with less than 20% down and that buyers should compare the total projected payment on the Loan Estimate, not principal and interest alone.

Boulder prices vary by property type, and nearby cities do not create one simple affordability ladder

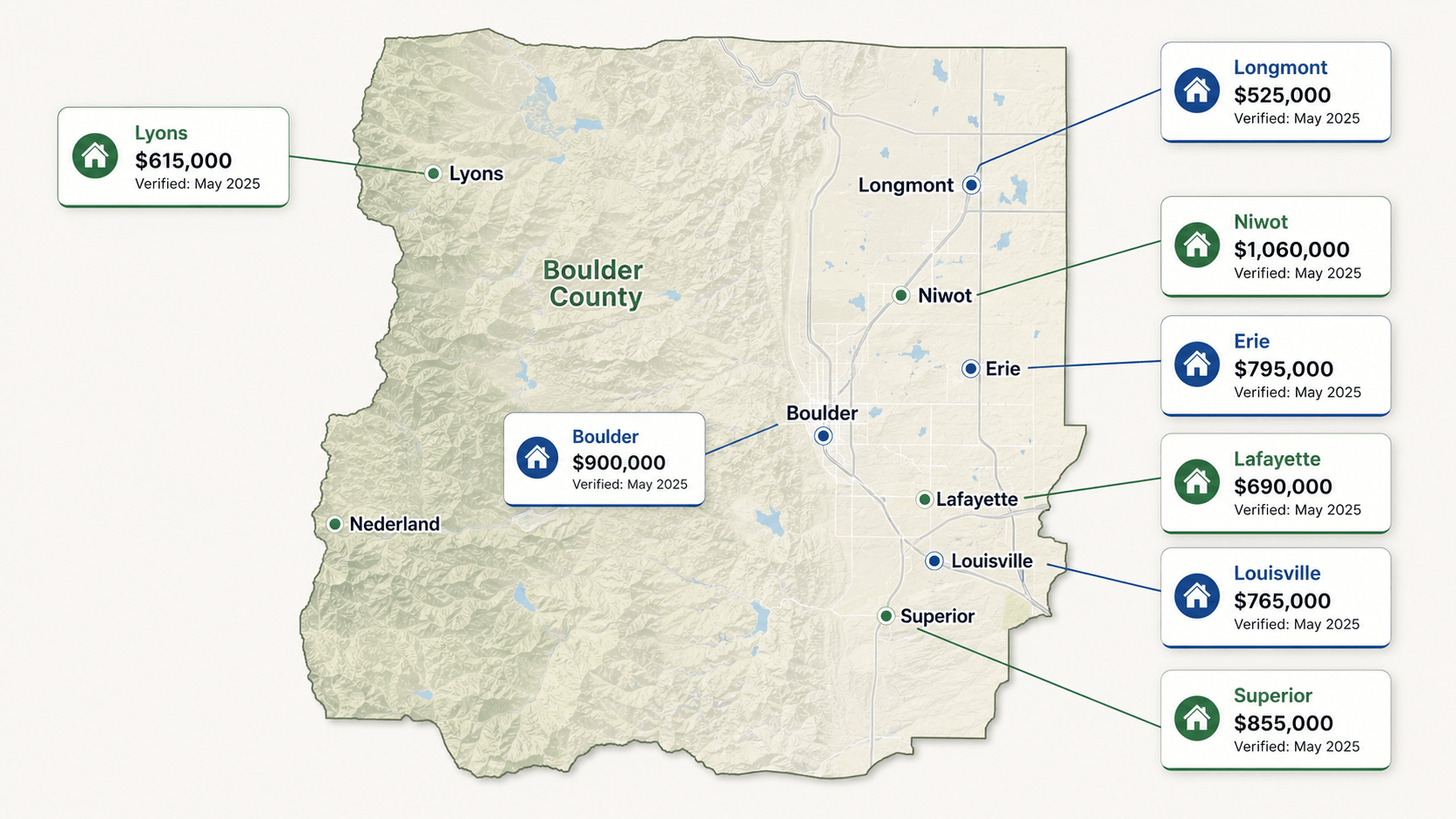

Boulder’s $854,489 figure is a median for all home types over the three months ending May 2026. It is not the price of a standard detached house, and it can move when the mix of condos, townhomes, luxury homes, and smaller properties changes. Over the same period, the Boulder County median was $747,757.

Broadening the search can change the income target. Longmont’s three-month median was about $554,668 and Lafayette’s was about $689,587 for the period ending May 2026. Those figures suggest that some buyers can lower the required payment by looking east or northeast, but the result depends on property type, exact location, HOA structure, commute needs, and insurance.

The practical local comparison is not simply “Boulder versus the suburbs.” Use the same criteria for every candidate property:

- Purchase price and likely loan amount

- Property taxes for the parcel and taxing districts

- Homeowners or condo-owner insurance quote

- HOA dues, reserve funding, and known special assessments

- Transportation costs and commute pattern

- Age, condition, near-term repairs, and energy use

- Floodplain, drainage, wildfire, and access considerations

Within Boulder itself, a central condo, a North Boulder townhome, a detached South Boulder house, and a foothills property can produce very different monthly costs even when list prices appear similar.

Within Boulder County, Longmont, Louisville, Lafayette, Superior, Erie, Niwot, Lyons, Nederland, and unincorporated areas also differ in housing stock, utilities, taxing districts, road access, and HOA prevalence. The correct comparison is property by property, not city label by city label.

Taxes, insurance, HOA dues, hazards, and loan type can change the income answer

The purchase price is only the starting point. In Boulder, the following items deserve an address-specific check before a buyer treats an income estimate as reliable.

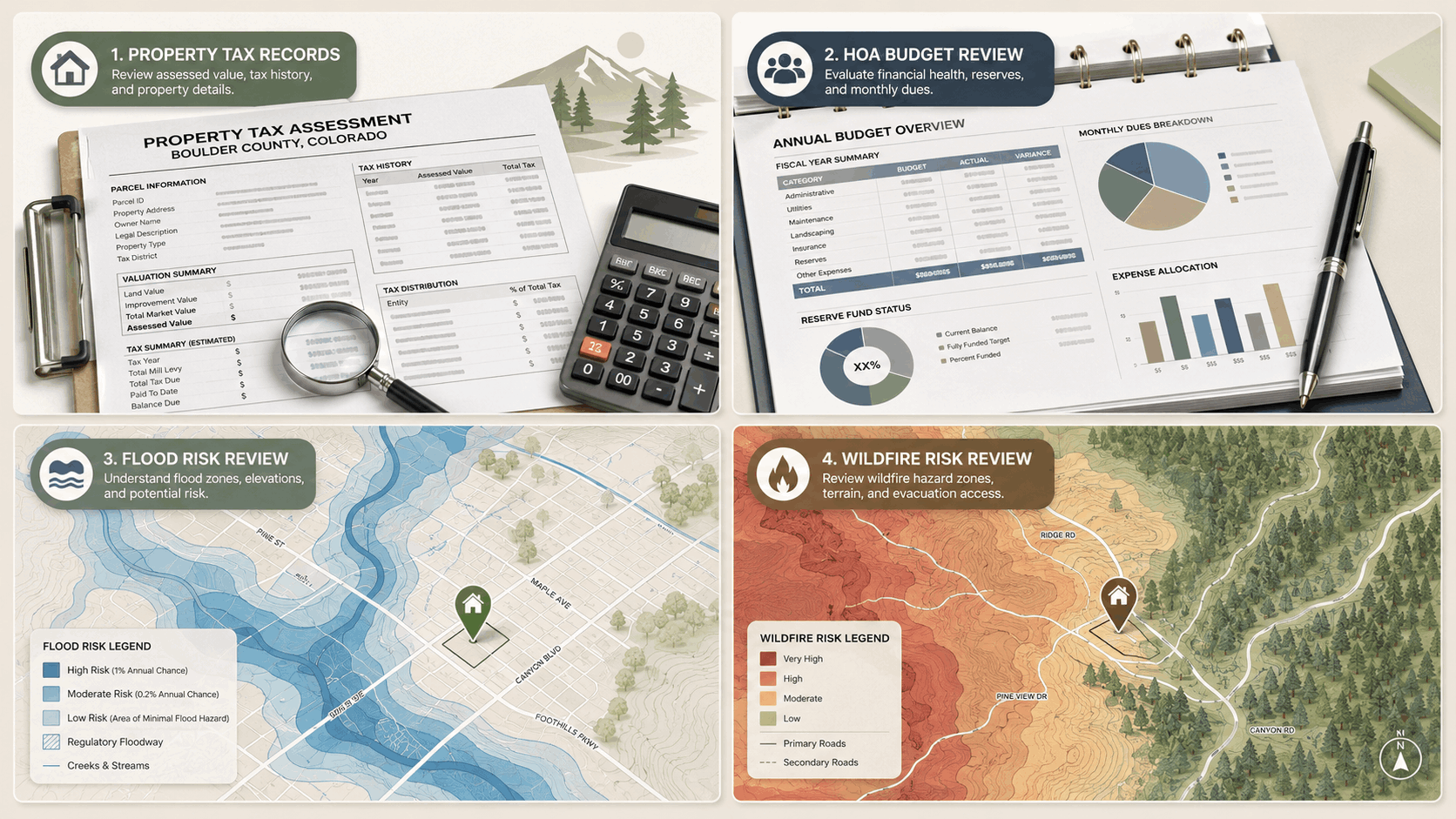

Property taxes

Boulder County calculates tax from actual value, the applicable assessment rate, and the mill levies for the property’s taxing districts. For tax year 2025, payable in 2026, the county’s illustration shows $4,942 of tax on an $800,000 residential property using assumed school and local-government mill levies. The county expressly identifies that as an example and directs owners to the Treasurer for an accurate calculation.

Do not apply a countywide percentage to a specific listing without checking the current tax record, assessed value, and district levies. New construction, reassessment, exemptions, and metropolitan or special districts can change the result.

Insurance, flood, and wildfire

Obtain an insurance quote for the exact address during the contract period, preferably before the insurance objection deadline. The City of Boulder provides an interactive floodplain map and can supply formal property floodplain information.

Boulder County’s wildfire program states that, as of July 1, 2026, unincorporated Boulder County is divided into three wildfire zones. Those maps are due-diligence tools; an insurer still determines availability, coverage, deductibles, and premium.

For condos and townhomes, review both the association’s master policy and the owner’s required policy. A high master-policy deductible or inadequate loss-assessment coverage can create meaningful out-of-pocket exposure even when monthly dues appear reasonable.

HOA and property condition

HOA dues belong in the monthly affordability calculation. So do pending special assessments and projects that may increase dues. Review the budget, reserve study if available, recent meeting minutes, insurance declarations, litigation disclosures, and maintenance responsibilities.

Detached homes need a separate repair and reserve plan. Older Boulder housing may require closer review of roofs, sewer lines, electrical systems, drainage, foundations, energy performance, and unpermitted work.

Foothills and mountain properties may add wells, septic systems, private roads, access, retaining structures, or wildfire mitigation to the due-diligence list. An inspector, engineer, insurer, lender, attorney, or other specialist should evaluate issues outside a real estate broker’s expertise.

Conforming versus jumbo financing

The official FHFA 2026 county file lists a $879,750 one-unit conforming loan limit for Boulder County. A loan above that amount is generally jumbo financing, which may carry different reserve, credit, appraisal, down-payment, and pricing requirements.

That is why the $1.25 million scenario above uses 30% down and an $875,000 loan for a cleaner conforming-loan illustration. Confirm the applicable limit and loan classification with the lender.

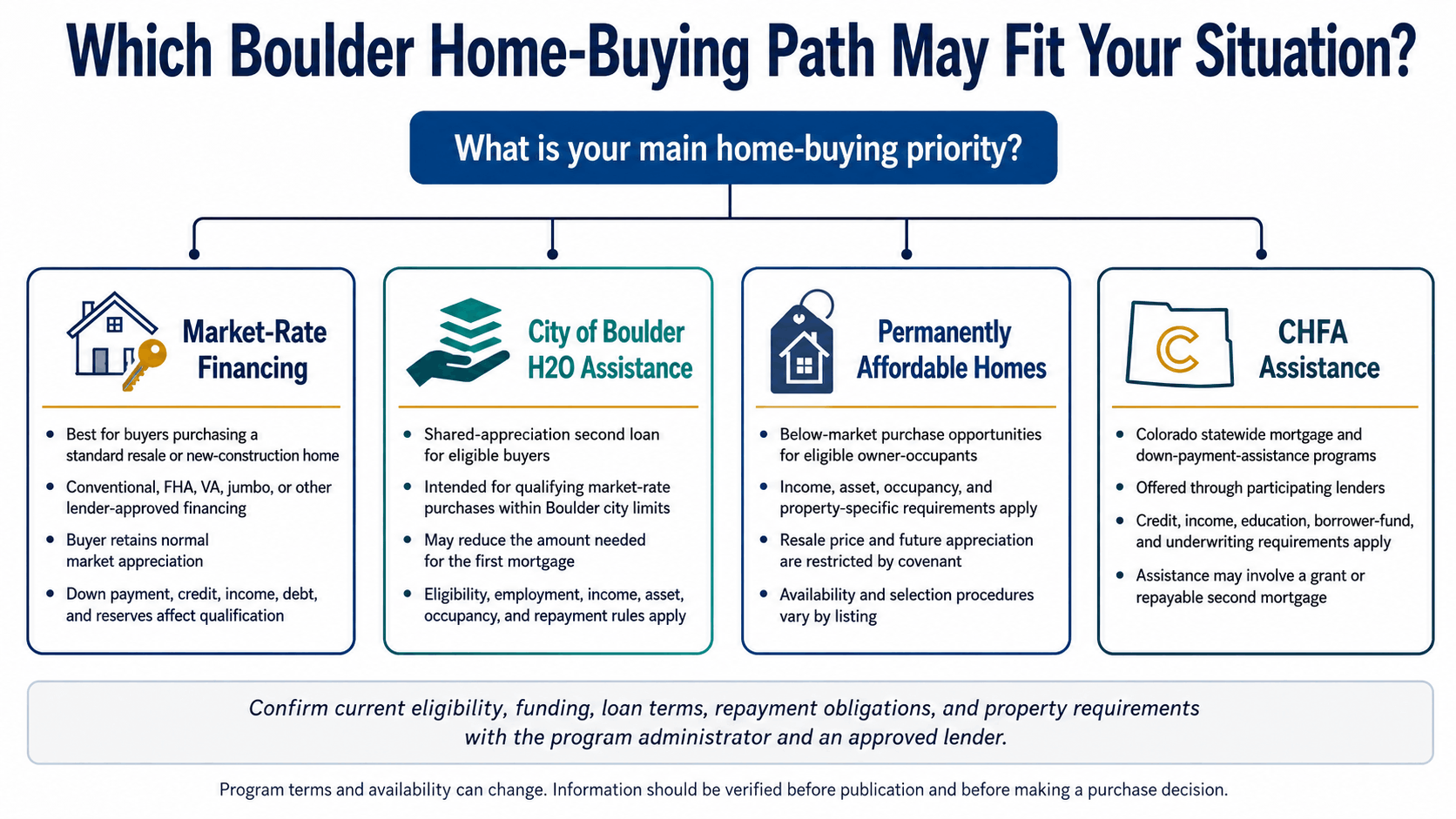

Boulder and Colorado buyer programs can reduce cash needs, but each has tradeoffs

Assistance programs may make a purchase possible with less cash, but they do not automatically make the ongoing payment affordable. Review the interest rate, second-lien terms, shared appreciation, resale restrictions, income limits, occupancy rules, and program funding status.

City of Boulder H2O program

As of July 2026, the House to Homeownership program offers eligible first-time buyers a shared-appreciation second loan of up to $100,000 for a market-rate home inside Boulder city limits. The city states that funds are limited and first-come, first-served.

Current requirements include working in the city, income and asset qualification, owner occupancy, homebuyer education, first-mortgage qualification, and a total DTI that should not exceed 45%. The published 2026 income maximum is $126,000 for one person and $144,000 for two people.

A full $100,000 reduction in the first mortgage would lower principal and interest by about $632 per month in a hypothetical 6.49% 30-year calculation. The H2O loan itself is deferred, but the principal plus a share of appreciation becomes due under the program terms. Compare the long-term equity tradeoff, not just the initial payment.

Boulder Regional Affordable Homeownership Program

Permanently affordable homes sell below market rate to income-eligible owner-occupants and carry an affordability covenant that limits resale price and imposes other restrictions. Each home has its own income limit, and many are below the published maximum.

For 2026, the city lists maximum income of $126,600 for one person, $180,000 for two people, and $225,000 for four people; the program also states that total DTI should not exceed 42%. Buyers must verify the listing-specific limit, asset rules, selection process, HOA dues, and resale covenant.

CHFA programs

The Colorado Housing and Finance Authority offers assistance through participating lenders. As of July 2026, its grant is up to the lesser of $25,000 or 3% of the first mortgage, while its second-mortgage option is up to the lesser of $25,000 or 4%. CHFA notes that higher rates apply to the assistance options.

General requirements include a mid-credit score of at least 620, applicable income limits, homebuyer education, at least $1,000 of borrower funds, and approval under the participating lender’s underwriting rules.

Program details change. Confirm eligibility, available funds, rates, repayment triggers, approved lenders, property rules, and compatibility with other assistance before relying on any program in an offer strategy.

Build a property-specific buying number before touring seriously

The most reliable Boulder home-buying budget is a worksheet built from a lender’s current quote and the actual properties you may pursue. Use this sequence:

- Set a comfortable monthly ceiling. Start with household cash flow, savings goals, taxes, benefits, childcare, transportation, and lifestyle spending rather than the largest payment an automated approval might allow.

- Obtain a fully underwritten or well-documented preapproval. Ask the lender to show the interest rate, APR, loan type, cash-to-close, projected taxes and insurance, mortgage insurance, and total monthly payment.

- Price each property separately. Pull the current tax record, obtain an insurance quote, confirm HOA dues and assessments, and estimate near-term repairs. For attached housing, review the association’s budget, reserves, insurance, and governing documents.

- Protect reserves. Down payment is not the only cash need. Keep funds for closing costs, moving, immediate repairs, deductibles, and an emergency reserve.

- Compare locations using the same worksheet. A lower-priced home in Longmont or Lafayette may improve the payment, while a Boulder condo may reduce purchase price but add HOA dues. A foothills property may require a different insurance and maintenance plan. Run the numbers instead of relying on citywide averages.

Before purchasing, independently verify school boundaries, zoning, permits, property condition, utilities, HOA obligations, floodplain status, wildfire information, insurance availability, taxes, and any rental or occupancy restrictions that matter to the property. Online estimates cannot replace a lender’s underwriting, an insurance quote, an inspection, title and HOA review, or advice from qualified legal, tax, engineering, environmental, or financial professionals.

For a property-specific affordability discussion, you can contact Eric Farran at Eric Sells Boulder. Eric can help compare current Boulder and Boulder County listings, identify the documents and local cost inputs to collect, and coordinate the real estate side of the process with your lender and other specialists.

The goal is not to stretch to a generic approval amount; it is to understand what a particular home would cost and what due diligence it requires before you commit.

Categories

Recent Posts