Boulder Condo & Townhome Buyer Guide: HOA Fees, Insurance, Reserves, and Hidden Costs

Buying a condo or townhome in Boulder can be a smart way to enter the market, reduce maintenance, or stay close to trails, schools, downtown, CU Boulder, or major Front Range employers. The key is understanding the full cost of ownership—not just the purchase price, but HOA dues, insurance responsibilities, reserve funding, rules, rental restrictions, and future special assessments.

For many buyers relocating to Boulder, Louisville, Lafayette, Longmont, Superior, Erie, Broomfield, or other Boulder County communities, attached housing can offer a practical balance of location, lifestyle, and budget. But every HOA is different, and the documents deserve as much attention as the inspection.

Key Takeaways for Boulder Condo and Townhome Buyers

A Boulder condo or townhome may be a good fit if you want a lower-maintenance property, shared exterior upkeep, and access to established neighborhoods where single-family homes may be harder to reach. HOA fees are not automatically “bad”—they often pay for real services such as exterior maintenance, landscaping, snow removal, common-area insurance, amenities, and reserve funding.

The biggest buyer mistake is comparing two properties only by list price or monthly payment. A lower-priced condo with a poorly funded HOA, high insurance deductible, aging roof system, or pending assessment may be more expensive long-term than a slightly higher-priced property in a well-run association.

In Colorado, many condos, townhomes, and planned communities are governed by homeowner association documents under the Colorado Common Interest Ownership Act, commonly called CCIOA. The Colorado Division of Real Estate’s HOA Center provides consumer information about HOA rights, responsibilities, and governing documents.

Best For / Not Ideal For

Condos and Townhomes May Be Best For

Boulder-area condos and townhomes often work well for first-time buyers, relocating professionals, CU Boulder families, downsizers, lock-and-leave owners, and buyers who want to live near walkable districts such as Downtown Boulder, Boulder Junction, Louisville’s Main Street area, Lafayette’s Old Town, or parts of Longmont and Broomfield.

They can also be a practical fit for buyers who want less yard work or who travel frequently. In some communities, the HOA handles exterior items that would otherwise fall directly on the homeowner.

Condos and Townhomes May Not Be Ideal For

Attached housing may not be the right fit if you want maximum control over exterior changes, parking, pets, rentals, landscaping, or future renovations. It may also be less ideal if the HOA has weak reserves, frequent special assessments, unresolved litigation, restrictive rental rules, or insurance coverage that creates large out-of-pocket risk for owners.

Understanding Boulder HOA Fees

HOA fees are monthly or periodic assessments paid by owners to fund the association’s operations. In Boulder County, HOA dues may cover different items depending on whether the property is a condo, townhome, patio home, or planned community.

Common HOA-covered items can include exterior maintenance, roof replacement, building insurance, landscaping, snow removal, trash service, water or sewer, common-area utilities, professional management, pool or clubhouse maintenance, elevator service, parking structures, reserves, and administrative costs.

The important question is not simply, “How much are the HOA dues?” The better question is, “What do the dues cover, and what remains my responsibility?”

For example, one Boulder condo HOA may include exterior building insurance, water, trash, snow removal, and roof reserves. Another association may have lower dues but leave more responsibility to the owner. In Louisville, Lafayette, Longmont, Erie, Superior, and Broomfield, newer townhome communities may offer lower exterior-maintenance needs at first, but buyers still need to understand how roofs, siding, fencing, alleys, shared drives, and landscaping will be funded over time.

Condo vs. Townhome: Why the Legal Structure Matters

Buyers often use “condo” and “townhome” interchangeably, but they are not always the same legally or financially. A condominium usually means the owner owns the interior unit and a shared interest in common elements. A townhome may include ownership of the structure and land beneath it, but that depends on the recorded documents.

This distinction affects insurance, maintenance, lending, appraisal, and resale. A row-style townhome in Boulder County might feel like a single-family home, but the HOA may still control exterior paint, roofing, fencing, parking, landscaping, and rental use. A condo near CU Boulder, downtown, or Boulder Junction may have more shared systems, such as hallways, roofs, elevators, boilers, or parking garages.

Before writing an offer, buyers should understand exactly what they own, what the HOA owns, and what maintenance obligations transfer with the property.

HOA Documents Buyers Should Review Carefully

Colorado real estate brokers use Colorado Real Estate Commission-approved contracts and forms when appropriate to the transaction. The Colorado residential contract includes provisions related to common interest community documents, and the contract language warns buyers to investigate the financial obligations of association membership.

A serious Boulder condo or townhome buyer should review:

- Declaration or CC&Rs

- Bylaws and rules and regulations

- Current budget

- Recent financial statements

- Reserve study, if available

- Meeting minutes

- Insurance declarations and master policy details

- Special assessment notices

- Litigation disclosures

- Rental restrictions

- Pet, parking, storage, and architectural rules

- Maintenance matrix showing owner vs. HOA responsibility

Meeting minutes are especially useful because they show what the community is actually discussing. Look for roof concerns, insurance premium changes, drainage issues, deferred maintenance, owner disputes, parking problems, upcoming capital projects, or repeated budget shortfalls.

HOA Reserves: The Long-Term Health of the Association

Reserves are funds set aside for major future repairs and replacements. For a condo or townhome HOA, reserves may be used for roofs, siding, asphalt, sidewalks, elevators, retaining walls, fencing, common plumbing, exterior paint, drainage systems, clubhouses, and other shared assets.

In Boulder County, reserves matter because building systems age, weather is hard on exterior materials, and labor and construction costs can be meaningful. Hail, freeze-thaw cycles, intense sun, wind events, and wildfire mitigation needs can all affect long-term maintenance planning.

A well-funded HOA does not eliminate risk, but it usually gives owners more predictability. A poorly funded HOA may keep monthly dues artificially low, only to rely on special assessments when large projects come due.

When reviewing reserves, ask these questions:

Does the HOA have a recent reserve study? Are monthly dues contributing to reserves? Are major projects expected soon? Has the association postponed necessary work? Do meeting minutes mention concerns about insurance, roofs, decks, drainage, or structural repairs?

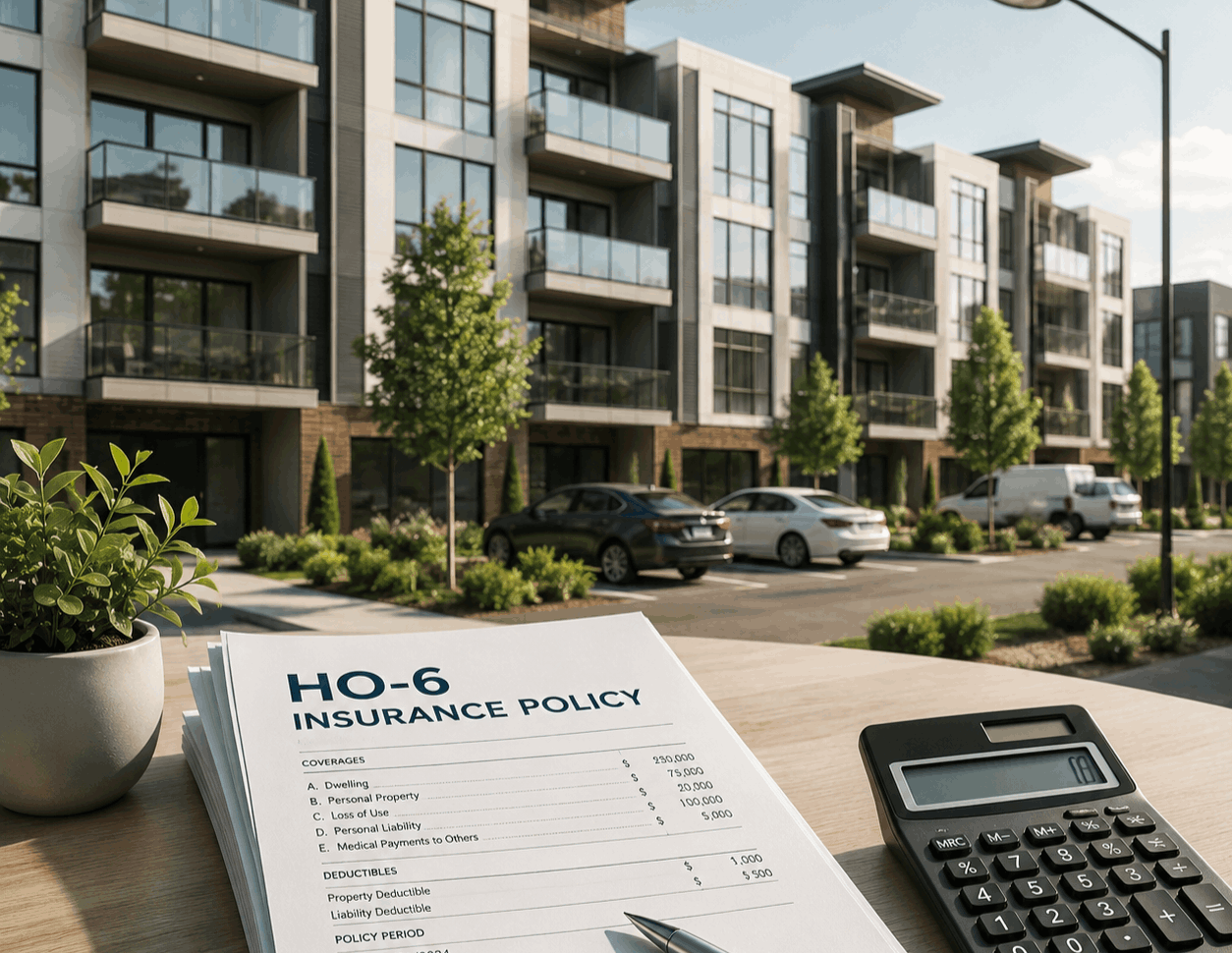

Insurance: Master Policy vs. Owner Policy

Insurance is one of the most important—and most misunderstood—parts of buying a condo or townhome. In many attached communities, the HOA carries a master insurance policy for certain building or common-area risks. The owner may still need a separate policy, often called an HO-6 policy for condos, to cover personal property, interior finishes, liability, loss assessment exposure, and other items.

Buyers should not assume the HOA’s policy covers everything. The real issue is the boundary between the association’s coverage and the owner’s coverage. That boundary may depend on the governing documents, the master policy, and the type of property.

In Boulder County and the Front Range, buyers should also pay close attention to deductibles, wind and hail coverage, wildfire exposure, water losses, and whether the association has discussed rising premiums. For foothills or wildland-urban interface locations, wildfire awareness is especially important. Boulder County provides wildfire mitigation guidance, and Wildfire Partners is Boulder County’s wildfire mitigation program for residents.

Before the inspection period ends, buyers should speak with an insurance professional and ask for a quote based on the actual property and HOA insurance documents.

Hidden Costs Buyers Often Miss

The purchase price and HOA dues are only part of the total cost. Boulder-area condo and townhome buyers should also budget for:

Special assessments for major repairs

Move-in or transfer fees

Capital contribution fees

Parking or storage fees

Higher insurance deductibles

Interior maintenance not covered by the HOA

Appliance replacement

Window and door responsibilities

Deck or patio maintenance

Rental license costs if used as an investment

Utility costs not included in dues

Pet fees or restrictions

Future HOA dues increases

For investment-minded buyers, City of Boulder rental rules can be especially important. Long-term rental properties in Boulder generally require rental licensing, and SmartRegs is part of the city’s rental compliance process.

The best time to discover these costs is before the HOA document deadline, not after closing.

Local Boulder County Considerations

Boulder is not one uniform market. A condo near Pearl Street, a townhome in North Boulder, a student-oriented unit near CU, a lock-and-leave property in Louisville, a newer townhome in Erie, and an attached home in Broomfield can have very different ownership considerations.

In central Boulder, buyers often prioritize walkability, bike access, transit, and proximity to restaurants, trails, and CU. In Louisville and Lafayette, buyers may compare small-town feel, schools, commuting routes, and newer attached-home options. Longmont may offer more space and a different price-to-location tradeoff. Superior and parts of Broomfield appeal to buyers who want access to Boulder and Denver corridors. Erie may attract buyers looking for newer construction and community amenities.

Floodplain review is also important in Boulder. The City of Boulder provides an interactive floodplain map, and buyers should verify whether a property is located in a mapped floodplain before committing.

How Sellers Should Think About HOA Documents

This article is written for buyers, but sellers should pay attention too. If you are selling a Boulder condo or townhome, clean HOA documentation can help reduce friction once you are under contract.

Before listing, gather current HOA dues, rules, insurance information, meeting minutes, reserve details, special assessment information, and transfer fees. If there is an upcoming assessment, insurance change, rental restriction, or major repair project, discuss disclosure strategy with your agent early.

A well-prepared seller can answer buyer questions quickly and keep the transaction moving. A seller who waits until contract deadlines are approaching may create uncertainty, delay, or avoidable buyer objections.

Practical Buyer Checklist Before You Commit

Before you buy a condo or townhome in Boulder County, take time to verify the details:

Review the HOA budget, reserves, and recent meeting minutes. Confirm what the dues cover. Ask whether any special assessments are pending. Review insurance deductibles and owner coverage needs. Understand rental, pet, parking, and renovation restrictions. Confirm who maintains roofs, windows, decks, fences, driveways, and exterior surfaces. Check floodplain, wildfire, and drainage considerations when relevant. Compare total monthly cost, not just purchase price. Speak with a lender familiar with condo and townhome financing. Speak with an insurance professional before your objection deadlines.

This is where experienced local guidance matters. The right property can be a strong long-term fit. The wrong HOA can turn an otherwise attractive home into a frustrating ownership experience.

Final Thoughts

A Boulder condo or townhome can be a smart move for the right buyer, especially if you value location, lower maintenance, and access to the Boulder County lifestyle. But the HOA is part of what you are buying. Its finances, rules, insurance, reserves, and maintenance culture can affect your monthly budget, resale value, and day-to-day experience.

If you are comparing condos or townhomes in Boulder, Louisville, Lafayette, Longmont, Superior, Erie, Broomfield, or the greater Front Range, Eric Farran can help you evaluate the property, the neighborhood, and the association details before you make a decision.

For local guidance, schedule a buyer consultation with Eric Farran and get a clearer view of what ownership will really look like before you write an offer.

Categories

Recent Posts